What Is Gap Insurance and What Does It Cover?

Gap insurance is short for Guaranteed Asset Protection and kicks in when your car is totaled, and the loan balance exceeds the car's market value, essentially covering the "gap" on the loan.

MF

By Mark Fitzpatrick

MF

Head of Insurance, MoneyGeek

Mark Fitzpatrick is a Licensed Property and Casualty Insurance Producer and MoneyGeek's Head of Insurance. He has analyzed the insurance market for over five years, conducting original research and creating personalized content for every kind of buyer. He has been quoted in several insurance-related publications, including [CNBC](https://www.cnbc.com/2020/04/15/cant-keep-up-with-insurance-premiums-heres-what-to-do.html), [NBC News](https://www.nbcnews.com/business/autos/flooded-cars-are-problem-their-owners-future-car-buyers-n1278493) and [Mashable](https://mashable.com/article/tesla-insurance-rates). Fitzpatrick earned a master’s degree in economics and international relations from Johns Hopkins University and a bachelor’s degree from Boston College. He is passionate about using his knowledge of economics and insurance to bring transparency around financial topics and help others feel confident in their money moves.

VC

Edited by Victoria Copans

VC

Victoria Copans is a professional writer, editor and translator. She previously worked as the managing editor for online events industry publication XLIVE. As a self-described budgeting nerd, she was drawn to the personal finance space to help share important and useful information that people may not otherwise have access to. In her free time, she loves to travel, learn languages and explore the beautiful nature in her home of Vermont.

MF

By Mark Fitzpatrick

MF

Head of Insurance, MoneyGeek

Mark Fitzpatrick is a Licensed Property and Casualty Insurance Producer and MoneyGeek's Head of Insurance. He has analyzed the insurance market for over five years, conducting original research and creating personalized content for every kind of buyer. He has been quoted in several insurance-related publications, including [CNBC](https://www.cnbc.com/2020/04/15/cant-keep-up-with-insurance-premiums-heres-what-to-do.html), [NBC News](https://www.nbcnews.com/business/autos/flooded-cars-are-problem-their-owners-future-car-buyers-n1278493) and [Mashable](https://mashable.com/article/tesla-insurance-rates). Fitzpatrick earned a master’s degree in economics and international relations from Johns Hopkins University and a bachelor’s degree from Boston College. He is passionate about using his knowledge of economics and insurance to bring transparency around financial topics and help others feel confident in their money moves.

VC

Edited by Victoria Copans

VC

Victoria Copans is a professional writer, editor and translator. She previously worked as the managing editor for online events industry publication XLIVE. As a self-described budgeting nerd, she was drawn to the personal finance space to help share important and useful information that people may not otherwise have access to. In her free time, she loves to travel, learn languages and explore the beautiful nature in her home of Vermont.

Updated: May 20, 2024

Advertising & Editorial Disclosure

Gap insurance comes into play when your car is totaled or stolen, and you owe more on it than its current value. Unlike standard auto insurance, which only covers your car's current value, gap insurance covers the extra amount you owe. It fills in this financial "gap," ensuring you're not stuck paying off a loan for a car you no longer have.

Gap insurance is an add-on to your regular auto insurance, not a replacement for it. So, it works alongside your standard coverage to give you full financial protection in specific situations.

Why Trust MoneyGeek? We ensure that MoneyGeek's content meets our highest editorial standards by carefully scrutinizing it. Throughout each stage, our team writes, checks facts, edits and reviews the content produced to generate accurate information.

Gap insurance, which stands for Guaranteed Asset Protection, is a type of auto insurance coverage designed to financially protect drivers if their car is totaled or stolen and they owe more on the loan than the car's current market value.

In such situations, gap insurance covers the difference, or "gap," between the two amounts. This ensures that you're not left with the financial burden of paying off a loan for a car you no longer have. Gap insurance is not a standard part of auto insurance — it's typically an additional coverage option that can be stacked on top of collision and comprehensive insurance within a full coverage car insurance policy.

This coverage type is usually only required by lenders or lessors. You do not need gap insurance if you own your car outright. The "gap" potentially exists between the loan amount and the car's current market value, so if you've bought your car without a loan or lease, there's no gap to worry about.

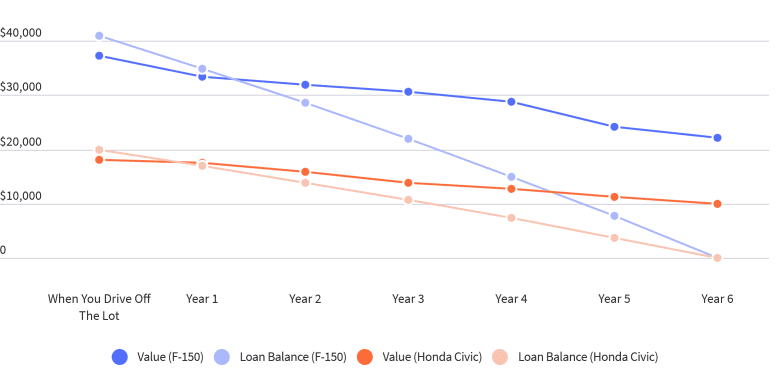

Illustrating Gap Insurance: Hypothetical Depreciation vs. Loan Balance

The graph above shows how gap insurance works with two different cars:

When you own a car, it's not just the initial cost that matters. As time goes by, your car's value decreases, but your loan balance often remains high. That mismatch can spell trouble if your car is in an accident or stolen, especially in the first few years of ownership. Your insurance payout might fall short of your outstanding balance, leaving you responsible for the difference, which can be substantial.

Gap insurance is your financial safety net, bridging the gap between your car's value and your remaining loan balance. If you ever find yourself "upside-down" on your loan and facing a car-related crisis, gap insurance steps in to save the day. Remember that the benefit goes to your financing company, ensuring your loan or lease is paid off so you can focus on getting back on the road without a heavy financial burden.

Gap insurance is especially useful for drivers who have recently financed a new car, have a long-term loan or have made a small down payment:

Why You Might Need Gap InsuranceYou’re a new car owner

The value of a new car depreciates quickly, often faster than you can pay down the loan. New cars can lose up to 20–30% of their value within the first year. If you've recently purchased a new car, gap insurance can protect you from potential financial fallout from the rapid depreciation, especially if you haven't made a significant down payment.

You have a long-term loan

Loans that extend beyond 60 months can create a situation where you owe more than the car's current market value for a longer period. Gap insurance can cover this difference, reducing your financial risk.

You’re leasing a car

Leasing contracts often require gap insurance as a protective measure. Since you don't own the car, the leasing company wants to ensure it won't incur a loss if the car is totaled or stolen.

You made a small down payment

A down payment of less than 20% can quickly lead to a situation where you owe more on the loan than the car is worth. Gap insurance can bridge this financial gap if your car is totaled or stolen.

You own a car with high depreciation

Some makes and models depreciate faster than others. If you own such a car, gap insurance can protect you from the financial shortfall that occurs if the car is totaled.

You’ve rolled over a previous loan

Rolling over a loan from a previous car into a new loan increases the likelihood of owing more than the car's value.

You may want to skip the gap coverage if:

However, keep in mind that you can only skip on this coverage if your lessor or lender does not require you to carry gap insurance.

A general formula to understand how gap insurance works could look like this:

Gap Insurance Coverage = Amount Owed on Loan or Lease - Car’s Current Market Value

When your car is totaled or stolen, your primary insurance (either collision or comprehensive, depending on the situation) will typically pay you the car's current market value. However, if you owe more on your loan or lease than that amount, you're left with a "gap" that you're still responsible for.

Standard auto insurance policies, like comprehensive and collision, cover your car's actual cash value (ACV), not what you originally paid for it. If your car is totaled or stolen, these policies will pay for repairs or a replacement based on its current value minus your car insurance deductible. For instance, if your car's current value is $4,000 and you have a $500 deductible, you'll get a payout of $3,500.

Gap insurance, on the other hand, fills in a specific financial gap. It won't pay for repairs or a new car; it simply covers the difference between your loan balance and the car's market value.

Below are three scenarios to illustrate how gap insurance works — all of these scenarios assume policies with no deductible.

Scenario 1: You financed a car

Amount Owed on Loan: $25,000

Car's Current Market Value: $20,000

Primary Insurance Payout: $20,000 (based on the car's current market value)

Gap Insurance Steps In:

In this case, your primary insurance would pay out $20,000, and the gap insurance would cover the remaining $5,000, allowing you to fully pay off your loan.

Scenario 2: You made a 10% down payment on a new car

Car's Initial Cost: $30,000

Down Payment: $3,000 (10% of $30,000)

Amount Owed on Loan: $27,000

Car's Current Market Value: $22,000

Primary Insurance Payout: $22,000

Gap insurance steps in:

Here, your primary insurance would pay out $22,000 based on the car's current market value, and the gap insurance would cover the $5,000 "gap," allowing you to fully pay off the loan.

Scenario 3: You leased a car

Amount Owed on Lease: $18,000

Car's Current Market Value: $15,000

Primary Insurance Payout: $15,000

Gap insurance steps in:

In this example, your primary insurance would pay out $15,000, and the gap insurance would cover the remaining $3,000, fulfilling your financial obligation to the leasing company.

Gap insurance only comes into play if your car is a total loss and you owe more on your loan than the car's current value. It won't help if your car isn't totaled or if you owe less than the car's worth.

Not all cars are eligible for gap insurance with every carrier. For example, high-end luxury or sports cars might not be covered. Also, the type of loan you have can affect your eligibility. Some carriers won't cover cars with specific loan types, like those with balloon payments or loans longer than 72 months.

You can get gap insurance coverage from your dealer or lender, a specialty carrier or from a third-party insurance provider.

Buy it from the car dealer or lender

How it Works: This is usually a lump-sum premium. The dealer pays the premium upfront and then rolls it into your loan, subject to your normal rate of interest.

Best For: People who prefer the convenience of one-stop shopping and are comfortable with the cost being bundled into their auto loan. However, be cautious, as the interest on your loan will also apply to this premium, making it more expensive in the long run.

Buy it from your own auto insurance company

How it Works: This option typically involves a monthly or six-month premium, added to your existing auto insurance bill. You won't be charged interest on it.

Best For: Those who prefer spreading out the cost over time without incurring interest. This is also a good option if you already have a strong relationship with your auto insurance provider and trust its services.

Buy it from a specialty gap insurance carrier

How it Works: This is also typically a lump-sum premium, paid upfront.

Best For: People who want a specialized focus on gap insurance, potentially offering more tailored options. This could be beneficial if you have a unique loan situation, like a very long-term loan or a loan with a high balance.

Dealer-sold gap insurance is almost always the most expensive option, by far. Buying gap insurance from your own insurance carrier has the advantage of a lower premium. Plus, since you’re paying monthly, you can cancel the coverage as soon as you’re no longer upside down on your loan. You may not have this option with lump-sum policies, especially when the premium has been rolled into your loan.

Ensure you're getting the best rate for your auto insurance. Compare quotes from the top insurance companies.